Best Ways to Exit Pre-Foreclosure in Dallas, TX Without Stress

Exiting a difficult housing situation in Dallas requires acting quickly before the bank moves toward a final sale. You can resolve this by catching up on payments through a reinstatement, selling the property to a cash buyer, or negotiating a short sale with your lender. Successful Pre-Foreclosure selling in Dallas, TX allows you to pay off the debt and protect your credit score from the long-term damage of a recorded foreclosure.

This guide provides a clear look at your options in the Texas real estate market. Professionals with years of experience in the Dallas-Fort Worth area have found that proactive communication with lenders is the most effective way to stop the clock. You will find practical steps here to manage your property debt and move forward with peace of mind.

1. Request a Loan Reinstatement from Your LenderHow Reinstatement Stops the Auction

A reinstatement is the fastest way to stop the process if you have access to a lump sum. You ask your lender for the total amount, including all missed payments, late fees, and legal costs. Once you pay this, your loan returns to its original standing.

Texas Specific Rights for Homeowners

In Texas, the law gives you specific rights during the early stages of a default. Many homeowners use a small inheritance, a personal loan, or savings to cover this cost. It is often the best choice if you want to keep your home and your financial setback was only temporary.

- Call your loan servicer immediately to get a formal reinstatement quote.

- Ask for a breakdown of all attorney fees added to the balance.

- Verify the payment deadline to ensure the foreclosure sale is canceled.

2. Pursue a Private Cash SaleBenefits of Selling Fast for Cash

Many homeowners choose to sell during pre-foreclosure because it offers a fast exit without the need for repairs. In Dallas, the market moves quickly, and cash buyers can often close in as little as seven days. This removes the stress of hosting open houses or waiting for a buyer to get bank approval.

Skipping the Repair Process

This method is particularly helpful if your house needs significant work. You won't have to spend money on paint, roofing, or flooring to get a fair offer. It allows you to walk away from the mortgage and potentially keep some equity for your next move.

- Look for local buyers who understand the Dallas County filing process.

- Request a proof of funds to ensure the buyer has the cash ready.

- Ensure the closing date is set at least a few days before the scheduled auction.

[Image: A professional meeting discussing real estate paperwork in a Dallas office setting]

3. Negotiate a Short Sale with the BankAsking the Bank to Accept Less

If you owe more than your home is worth, a short sale process might be your only way to avoid a foreclosure. This involves asking the bank to accept a lower amount than the total mortgage balance. While it takes longer than a cash sale, it is much better for your credit history than a foreclosure.

Proving Financial Hardship

Banks are often willing to do this to avoid the costs of seizing and selling the property themselves. You will need to provide financial documents proving hardship. This could include medical bills, proof of job loss, or a divorce decree.

- Hire an agent or lawyer who specializes in short sale negotiations.

- Prepare a hardship letter explaining why you can no longer afford the payments.

- Be patient, as banks can take several weeks or months to approve the deal.

4. Consider a Deed in Lieu of ForeclosureVoluntary Property Transfer

A deed in lieu is basically voluntarily handing the keys back to the bank. You sign the property over to the lender, and in exchange, they cancel the debt. This is a clean break that avoids the public embarrassment of a foreclosure auction on the courthouse steps.

Avoiding Deficiency Judgments

Bonus Tip: Before signing a deed in lieu, ask the lender if they will waive the "deficiency judgment." This prevents them from coming after you later for any remaining balance if the house sells for less than you owed.

- This option is usually only available if you cannot sell the home through other means.

- It requires the property to be free of other liens or secondary mortgages.

- The bank will inspect the home to ensure it is in acceptable condition.

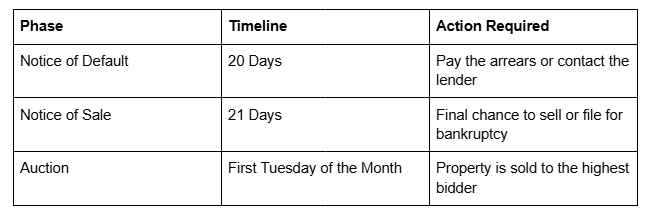

How does the Dallas foreclosure timeline work?Understanding Texas Foreclosure Laws

Texas is a non-judicial foreclosure state, which means the process moves faster than in many other places. Once you miss a payment, the lender sends a Notice of Default, giving you 20 days to fix the issue. If you don't, they can send a Notice of Sale, which gives you only 21 days before the auction.

5. Explore a Loan ModificationChanging the Terms of Your Mortgage

If you want to stay in the home but can't afford the current payments, a modification might help. The lender changes the terms of your original contract. They might lower the interest rate or extend the length of the loan to make the monthly cost more manageable.

Requirements for Approval

This requires a lot of paperwork and a trial period where you must make three on-time payments. It is a good long-term solution, but it requires a stable income. Selling a house in default is usually better if your income has permanently dropped.

- Submit a complete loss mitigation package to your lender.

- Follow up every few days to ensure no documents are missing.

- Continue making whatever payments you can during the review process.

Things to think about before choosing your exit strategyAssessing Your Home Equity

Before you decide on a path, you must consider your total debt and your home's current value. If you have significant equity, a traditional or cash sale is almost always the best financial move. If you have no equity, you must decide between a short sale or a deed in lieu.

Long Term Credit Impact

You should also think about your future housing needs. A foreclosure stays on your credit report for seven years and can make it very hard to rent an apartment or buy another home. Taking action now protects your ability to move on quickly.

- Calculate your "payoff amount," not just your current balance.

- Check for any secondary liens, such as HOA dues or tax debts.

- Assess the cost of moving and finding a new place to live.

Bonus Tip: Check the Dallas County property records to see if any other liens are attached to your title. Solving these early makes Pre-Foreclosure selling much smoother.

Get Expert Help to Avoid Foreclosure and Secure a Free Cash Offer Today

If you are feeling the pressure of a looming auction date, talking to a professional buyer can provide the clarity you need. Companies like OT Home Buyers specialize in helping Dallas homeowners move past difficult financial situations. They offer a direct way to settle your debt without the hassle of a traditional listing.

You can reach out to them to discuss your property and receive a no-obligation quote. By contacting Vince at 682-267-7741 or emailing [email protected], you get access to a team that understands the local Texas market. They can help you evaluate whether a cash sale is the right move for your specific goals. Taking this step allows you to control your future and avoid the long-term consequences of foreclosure.

Summary of your options in Dallas

When you face a default, your primary goal is to stop the auction and protect your financial reputation. Whether you choose a reinstatement, a loan modification, or Pre-Foreclosure selling, acting early is the most important factor. Dallas homeowners have multiple paths to a fresh start, provided they don't ignore their lender's notices. Evaluate your equity, check your timeline, and reach out to local experts who can guide you through the paperwork and closing process.

Common Questions About Property Default in TexasWhat is the fastest way to stop a foreclosure in Dallas?

Selling your home to a cash buyer is often the fastest method. They can close in days, providing the funds necessary to pay off the lender and cancel the scheduled auction immediately.

Can I sell my house if the auction is next week?

Yes, but you must act very fast. A cash buyer can often expedite the title work to close before the first Tuesday of the month, which is when Texas foreclosure auctions occur.

Does a short sale hurt my credit as much as a foreclosure?

No, a short sale is generally less damaging. While it will impact your score, it typically allows you to apply for a new mortgage much sooner than a recorded foreclosure would.

What happens if I just leave the house?

If you walk away, the bank will sell the property at auction. You may still be liable for a deficiency judgment if the sale price doesn't cover your debt, and your credit will be severely damaged.

Are there fees for getting a cash offer?

Reputable local buyers do not charge fees for making an offer. They typically cover all closing costs, allowing you to know exactly how much money you will walk away with.

AiraBreeze Portable Air Cooler: How It Works, Key Features, Benefits,...

AiraBreeze is a compact personal cooling device designed to provide refreshing airflow in...

Glucotex Blood Sugar Support : Tout ce qu'il faut savoir avant d'achet...

Glucotex est un complément alimentaire formulé pour aider à maintenir une glycémie saine,...